")

Cash to digital payments transition: Case studies of Japan, Germany, Brazil, and Mexico

16 May 2024 in Blog,Case Study

by Ludovic Plisson

Share This Story, Choose Your Platform!

The transition from cash to digital payments remains a critical topic in modern finance. Many countries advance their infrastructure and regulatory efforts to reduce cash reliance in favour of more efficient and secure digital solutions. This transition supports not only payment modernisation but also financial inclusion and economic dynamism. In this article we update the challenges and opportunities and revisit four country-cases: Japan, Germany, Brazil and Mexico, now with 2025 data and projections.

Global context of cash & digital payments

Current state worldwide

-

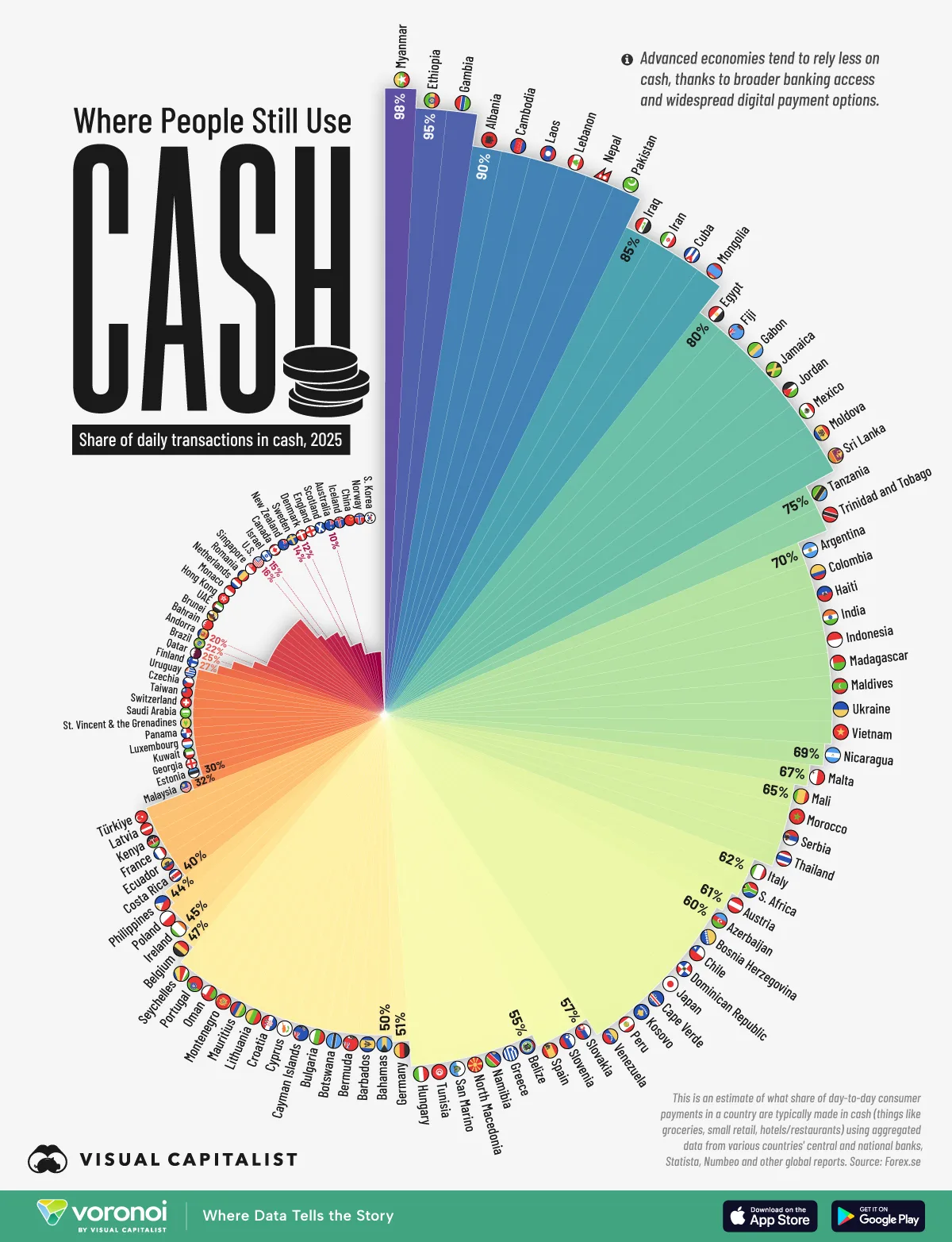

A recent ranking by Visual Capitalist shows that in 2025, many countries still see very high shares of daily transactions in cash (for instance Myanmar ~98 %). Visual Capitalist

-

The Bank for International Settlements notes: “The ongoing digitalisation of payments coincides with a further decline in cash in circulation. Even so, the demand for cash withdrawals has generally stabilised, which highlights the lasting role of cash.” Banque des Règlements Internationaux+1

-

According to the report “Global Payments Outlook 2025” by e‑MerchantPay, digital wallets are expected to account for over 40% of eCommerce transactions by 2025. emerchantpay

Key implications

-

Digital payments are clearly gaining ground, but cash remains structurally relevant.

-

The transition is uneven: by region, by demographic, by payment channel.

-

For payment infrastructure providers (PSPs, PayFacs, ISOs, ISVs) this means supporting hybrid environments: legacy cash flows + new digital rails.

Japan 🇯🇵 – from cash-heavy towards a cashless framing

Updated state (2024/25)

-

According to Japan’s Ministry of Economy, Trade and Industry (METI), the “cashless payment ratio” (i.e., share of amount paid by consumers via non-cash means) reached 42.8% in 2024, thus surpassing the government’s 40% target one year ahead of schedule. meti.go.jp+2GlobalData+2

-

A Reuters article confirms this progress: “cashless payments rising to 42.8% in 2024…”. Reuters

-

Projection: The longer-term government target is to reach ~80% cashless transactions (amount basis) in the future. meti.go.jp+1

Challenges

-

Cultural inertia: many consumers and small merchants still prefer cash because of familiarity, perceived trustworthiness and simplicity.

-

Infrastructure: large networks of vending machines, small independents, legacy ticketing systems still rely heavily on cash.

-

Older demographic: greater cash use persists in older age-bands.

Opportunities and solutions for digital payments

-

For a PayFac/PSP in Japan, the key is digital-onboarding of small merchants and QR/QR-code + mobile wallet adoption (e.g., PayPay, LINE Pay) in local commerce.

-

Payment infrastructure must support multi-method routing (card + QR + mobile wallet) and address offline / low-connectivity merchants.

-

Cash remains as fallback and resilience mechanism: so designing for hybrid (digital + cash) is prudent.

Germany 🇩🇪 – tradition meets transition

Key challenges

-

Data protection and trust: German consumers remain cautious about data privacy and digital payments.

-

Cash culture: Germany retains a significant cash‐preference, especially for smaller purchases and among older consumers.

-

Merchant cost/fees: merchants are still sensitive to card/acquirer fees and sometimes prefer cash for cost control.

Opportunities & solutions

-

Real-time payments (SEPA Instant) are an enabler: roll-out in 2025 will push the digital part of the stack.

-

For international PSP/PayFac targeting Germany, offering a unified stack that supports local preferences (EC / girocard, digital wallets like Apple Pay/Google Pay, instant bank transfers) is key.

-

Positioning “cashless” not as “no cash allowed” but as “digital first + cash fallback” will align with German preferences.

Brazil 🇧🇷 – leapfrog via instant payments

Updated state (2025)

-

The instant payment system Pix has become dominant: the Banco Central do Brasil reports that by early 2025, Pix was used by 76.4% of the population, followed by debit card at 69.1%, and cash by 68.9%. bcb.gov.br

-

While cash still has presence in Brazil, multiple sources indicate a steep decline in cash as the main payment method due to Pix. PagBrasil+1

-

A journalistic article notes that in April 2025 the volume transacted via Pix reached over R$2.677 trillion (~€410 billion) for the month, overtaking both card and cash payments. Le Monde.fr

Challenges

-

Rural & informal segments: Although Pix penetrates widely, some low-connectivity and informal merchants may still rely on cash.

-

Technology access/inclusion: Not all segments have smartphones or feel comfortable with QR/mobile wallets yet.

-

Infrastructure & cost: Merchant adoption may require updating POS/supporting QR acceptance.

Opportunities & solutions

-

For a payment infrastructure provider, Brazil offers a blueprint for rapid digital migration: instant payments, free for individuals, QR first, broad merchant adoption.

-

A “white-label infrastructure” that supports multiple local APMs (including Pix) and handles routing, fallback, tokenisation is a strong offering.

-

Use case: embedding instant payments into marketplaces, platforms, small merchants — converting what was previously cash-on-delivery.

Mexico 🇲🇽 – still cash-heavy but catching up

Key challenges

-

Large unbanked/under-banked population: many consumers still lack transaction accounts or digital-payment readiness.

-

Infrastructure gaps: rural areas and small merchants may lack POS devices, reliable connectivity, or awareness.

-

Consumer trust/habit: cash remains a default, especially for low-ticket, everyday purchases.

Opportunities and solutions

-

Accelerating mobile wallet and QR adoption: focusing on low-cost merchant devices, offline/agent models, low-ticket digital acceptance.

-

Incentives and consumer campaigns: rewards, cashback, loyalty tied to digital payments to shift behaviour.

-

Infrastructure approach: For ISVs and platforms in Mexico, offer a unified digital payments layer that supports local APMs, routing, tokenisation, and integrates with merchants that historically accepted cash.

Conclusion

The transition from cash to digital payments in 2025 is far from uniform. The cases show:

-

In developed markets like Japan and Germany, the shift is gradual and framed by tradition, culture and infrastructure legacy.

-

In emerging markets like Brazil (and to a lesser extent Mexico), digital adoption is more rapid when enabled by strong infrastructure (e.g., Pix) and supportive regulation.

-

For payment infrastructure providers (PSPs, PayFacs, ISVs), the winning strategy is not “eliminate cash overnight” but rather:

-

Support both cash and digital channels (hybrid)

-

Build routing, tokenisation and reconciliation layers to handle complexity

-

Leverage strong local APM adoption and be ready for rapid shifts

-

Use data and instrumentation to optimise flows, cost, fraud, and approval/settlement rates

-

In 2025 and beyond, cash will not disappear entirely, but digital first + cash fallback is the emerging norm. For infrastructure players, this means enabling scalability, flexibility, local-method coverage and resilience.